Using Testamentary Trusts to ensure your inheritance is protected for your family and does not…

Merthyr LawAugust 7, 2017

It’s not something anyone likes to think about, but estate and succession planning is essential if you want to ensure your family and business partners are protected when you’re no longer around.

At Merthyr Law, we make sure we understand your unique set of circumstances so we can offer expert advice and structure your affairs to keep your assets in the right hands.

Our Family Safe® Program ensures we regularly review your estate planning. As a result, we stay on top of any changes in your personal circumstances and make the necessary adjustments when there are changes in the law.

You owe it to your loved ones to keep your Family Safe by investing in an effective estate and succession plan rather than leaving them with your mess to sort out. And by making a clear plan, you can also protect your assets against attack from the family court or bankruptcy.

In addition, estate and succession planning effectively limits potential disputes among beneficiaries, helping to keep family feuds at bay.

Our online systems allow you to get started anywhere, any time.

Have a question?

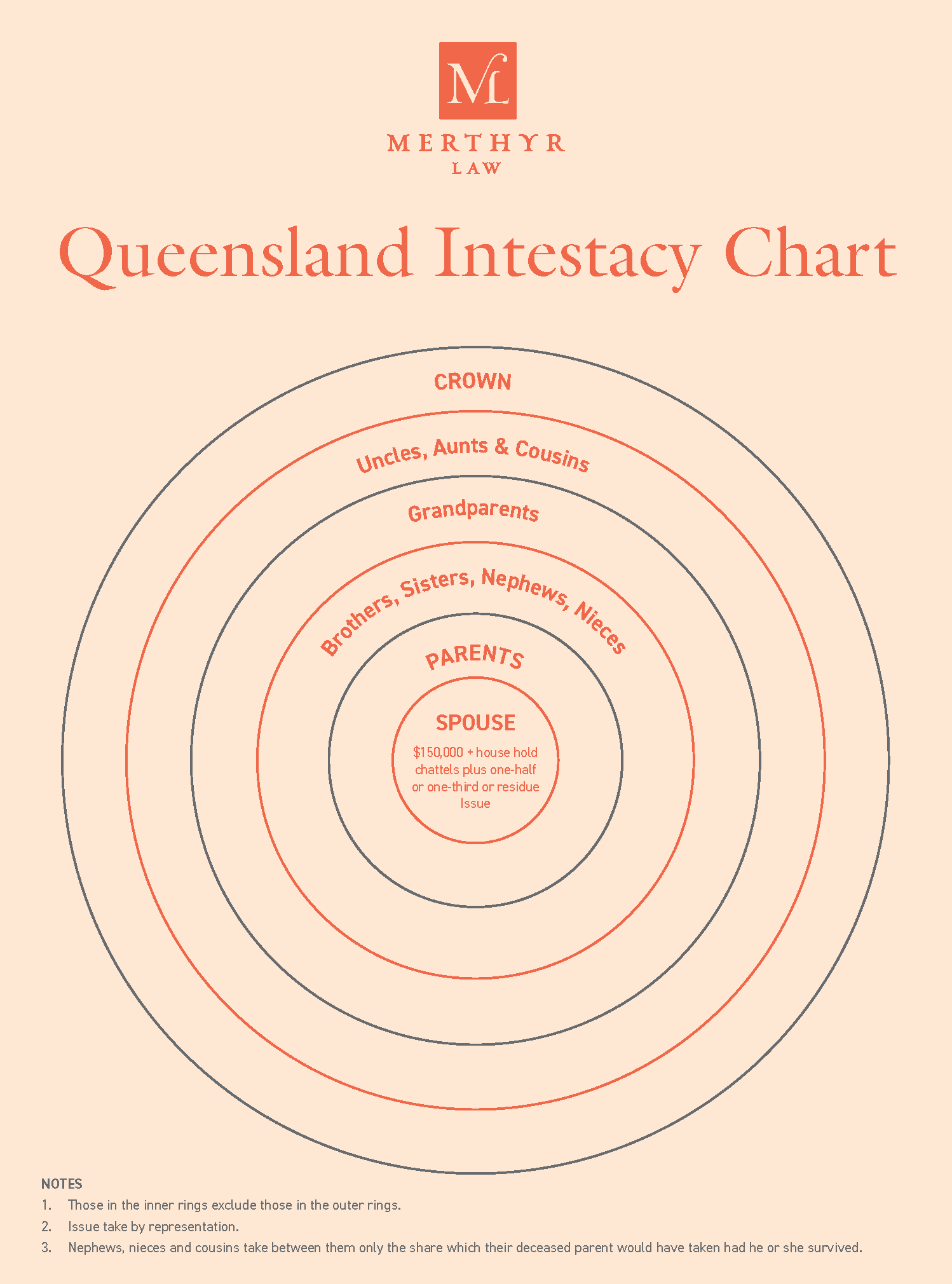

If you die without making a Will, your assets will be distributed according to a strict formula set down by the Law. This may mean

Creating a Will is not like fixing a car. You won’t get a chance to fix it once it breaks down and the consequences of a faulty Will can be disastrous for your loved ones, once you have gone. Your Will sets out:

If you don’t have a Will, you will not have a say in how your assets will be distributed and who distributes them.

Ten years ago, your most valuable single asset may have been your family home. Now, the lion’s share of your wealth is likely to be held within your superannuation fund. It’s easy to forget your superannuation, life insurance policies and other assets when thinking about your ‘estate’.

In addition, your self-managed superannuation needs special consideration to prevent non-compliance or adverse taxation consequences upon death.

Without an up-to-date Will that makes accommodation for these assets, they may never end up with the loved ones that you intended to have them. Everyone should prepare a Will for peace of mind and to ensure their wishes are fulfilled in the event of their death.

You can change your Will at any time you choose but there are certain circumstances that revoke your Will and others where it is strongly recommended that you review your Will.

A Power of Attorney is a written agreement recognised by law that gives someone else the power to sign documents and make decisions on your behalf. An Enduring Power of Attorney is an agreement that continues to have force even after you become incapable of making decisions for yourself. An Enduring Power of Attorney can empower the attorney to make decisions not only about financial matters but also personal matters which include:

You are able to nominate a trusted person or persons (often a family member) to be your attorney and can limit their powers when appointing them.

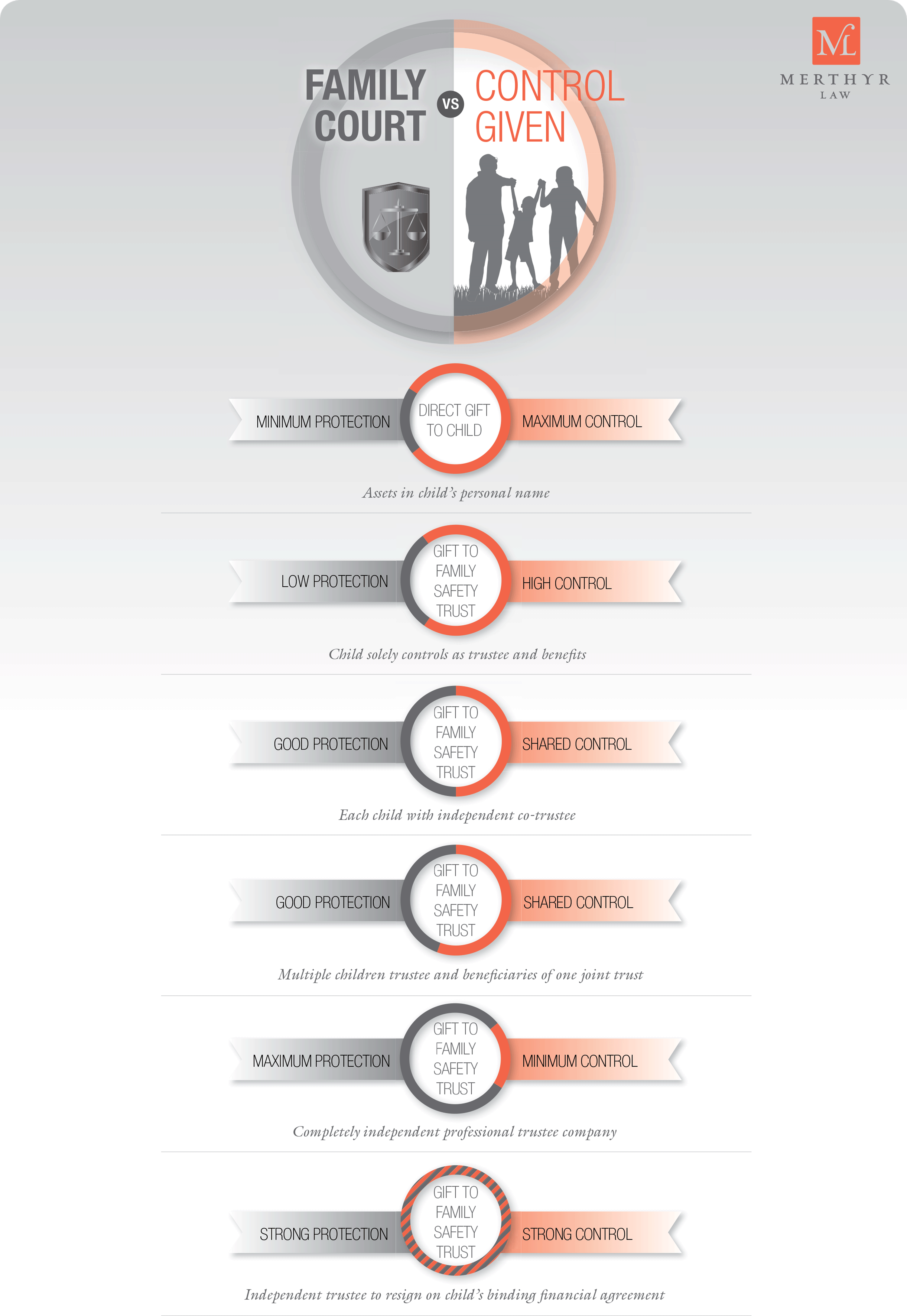

Generally, the more control a beneficiary has over their inheritance, the greater the risk of family law property adjustment. See our Family Court Protection Spectrum below.

Click image to enlarge

Yes. Minors sometimes are recipients of sizeable inheritances or personal injury awards. Minors do not have capacity to make a Will, and as such, if a minor dies the rules of intestacy apply, meaning that the minor’s inheritance is usually split equally between the surviving parents. If a person believes that the rules of intestacy lead to an unfair outcome, such person can apply to the Court for the Court to order a Statutory Will for a person.

Yes. This very circumstance happened in the case of RKC v JNS [2014] QSC 313 (link: https://archive.sclqld.org.au/qjudgment/2014/QSC14-313.pdf). In that case, the son was severely disabled from birth and was the recipient of sizeable personal injury compensation. The mother was responsible for the care of the disabled child and the father had little to do with the mother or the child. If the disabled child died without a Will, the inheritance would have been split equally between the father and the mother, despite the father having little to do with the child. In this case, the Court found that it was appropriate to order the disabled child to have a Statutory Will leaving all of his inheritance to the mother.

Yes. At risk business people wish to avoid accumulating wealth in their own name, as litigation may result in such wealth ending up with creditors.

Testamentary Trusts are often used as a vehicle to ensure that inheritances are protected from beneficiaries’ possible creditors and bankruptcy. In RE Matsis [2012] QSC 349 (link: http://www8.austlii.edu.au/cgi-bin/viewdoc/au/cases/qld/QSC/2012/349.html) the Court upheld an application by three sons who were financially at risk for their incapacitated mother’s Will be changed to one containing a testamentary trust.

Also, testamentary trusts can be used as a vehicle to help protect inheritances from the reach of the Family Court – see Family Court Protection Spectrum. Merthyr Law successfully made the first application to the Court for an incapacitated mother’s Will to be changed to a Will containing Testamentary Trusts in order to ensure that the mother’s inheritance did not end up with the daughter-in-law who had recently separated from the son and was involved in Family Court Property proceedings – see GUA v GAV [2014] QCA 308.

Sometimes everybody knows that there is going to be estate litigation between the children once the parents pass away. In circumstances where the surviving parent is incapacitated, Statutory Will arrangements, combined with a Deed of Family Arrangement, where the beneficiaries agree not to challenge the Will can be used as an effective means to help ensure there is a fair distribution between the children and to minimise the risk of estate litigation after the parent’s passing. NSW is the only jurisdiction that enables a person under section 95 of the Succession Act 2006 to release that person’s right to seek a Family Provision Order. As such, in NSW, it is possible for an incapacitated Will to be changed and for potential claimants to relinquish their right to make a Family Provision Claim in the one application – see Re RB, A Protected Estate Family Settlement [2015] NSWSC 70.

If the testator has never made a Will and no Statutory Will has been ordered, that person is called an “intestate” (meaning dying without a Will). The laws of intestacy in Queensland provide that an intestate person’s estate is distributed as follows:

Click image to enlarge

If the distribution on intestacy is reasonable in the circumstances and fairly likely to be what the Testator would have wanted, there ought to be no need to apply for a Statutory Will.

However, if the distribution on intestacy leads to a result that is not fair or not likely to be what the testator would have wanted had they had capacity, it may be worthwhile applying to the Court for a Statutory Will.

In this animated video series, Kieran Hoare of Merthyr Law covers strategies to help protect your legacy and keep your family safe.

© 2024 Merthyr Law. | Privacy Policy | Employee login | Site by Ruby Ink